Arvind Q1 review: Textile disappoints; branded apparel, engineering grow

Arvind, one of India’s biggest conglomerates, is engaged in businesses across verticals such as textiles (fabric and garment manufacturing cum sale), branded apparel retailing, engineering, home textiles (for infra, healthcare, energy, aviation clients) and water treatment.

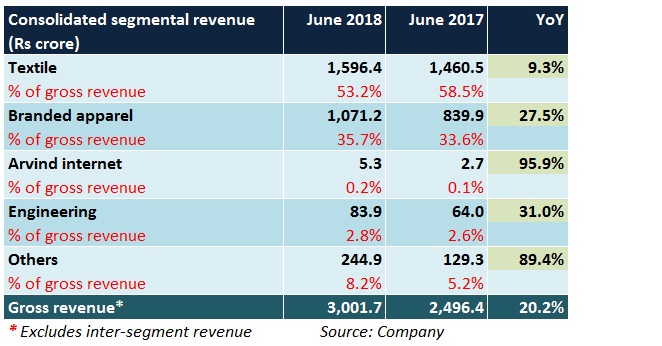

In Q1 FY19, the company’s consolidated top-line growth was tepid owing to the under performance of the textile segment, which constitutes nearly 50-55 percent of the total turnover. This was largely on account of a high base in Q1 FY18 (buyers preponed purchases prior to GST implementation from Q2) and a weak off take in denim fabrics. In contrast, robust year-on-year (YoY) revenue growth was observed in case of the other segments.

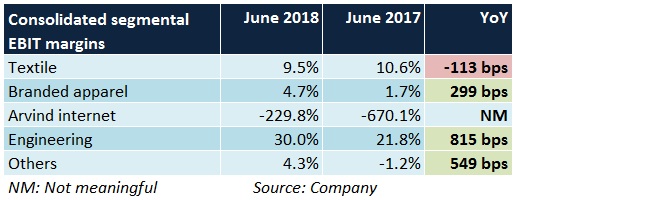

High raw material costs (cotton), prima facie, weighed in on Arvind’s gross margins significantly during the quarter, which, in turn, took a toll on the operating margins. From a YoY perspective, higher depreciation and financing costs (primarily on account of investments in the textile and branded apparel segments), coupled with an increase in tax rate, compressed the company’s profit margin.

The road ahead

Textile

In a bid to move up the textile value chain and earn better margins, Arvind is shifting its focus gradually from fabrics to garmenting. At present, garment manufacturing facilities are located in India and Ethiopia, with the latter catering exclusively to export markets in North America and Europe at zero rate of duty.

To expand its manufacturing base, the management intends to increase its capacity by 3 times in the next 3 years, mainly in Jharkhand and Ethiopia. Foray into new sub-segments such as activewear, sportswear, and loungewear (using synthetic fibres or a blend of cotton and synthetic material) is also on the agenda.

Currently, 10 percent of the fabric manufactured is used as an input for manufacturing garments. In the next 3-5 years, the management targets to take this number to 30-40 percent. Consequently, cost savings and reduced dependence on external suppliers should be margin accretive.

Branded apparel

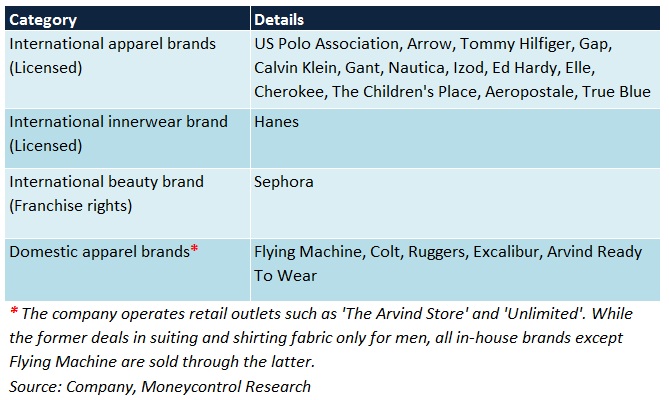

On the back of a strong portfolio of international and in-house brands, this segment is well-poised to maintain its consistent run in terms of revenue growth. An uptrend in sale volumes and higher realisations (especially in case of foreign brands) should help offset the corresponding increase in promotional spends, thus leading to operating leverage in due course.

3 international brands, that were loss-making in the past, are likely to turn profitable by the end of FY19 because of economies of scale. Since the contribution of this segment to Arvind’s annual turnover is sizeable (30-40 percent), the company’s overall margin profile will improve.

Given the high growth potential and good brand recall in this space, investments by way of store additions across retail channels (large format stores, multi-brand outlets, exclusive brand outlets) and marketing will pick up the pace going forward.

The manufacturing operations, however, will be predominantly outsourced to keep the business model asset-light. Furthermore, after this segment is listed as a separate entity (Arvind Fashions), product offerings will be extended to cover categories such as footwear (3 brands already in the kitty) and customised premium clothing under the ‘Creyate’ brand.

Engineering

This segment designs and manufactures critical process equipment (heat exchangers, pressure vessels, reactors, columns/towers, centrifuges, etc) for businesses operating in domains such as petrochemicals, fertilizers, and power, among others. Anup Engineering is the third largest heavy fabrication player in India.

To capitalise on the historically witnessed steady growth momentum (sales CAGR of 25 percent in FY13-18, margins of about 30 percent, return on capital employed of roughly 40 percent), Anup Engineering, an entity with a cash positive balance sheet, aims to explore opportunities in global markets. The management targets to reach the Rs 1,000 crore revenue mark over the next 5-7 years.

Advanced material (Technical textiles)

This segment’s revenue grew 10 percent YoY in Q1 FY19. Arvind’s management anticipates sales to grow by at least 20 percent every year and also foresees margins improving through operational efficiencies. Through continued investments at periodic intervals, the intent is to achieve a top-line of Rs 100 crore by FY20 end.

Should you invest?

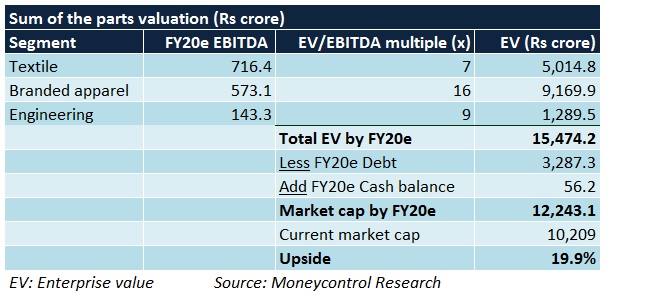

Proposed demerger of the branded apparel and engineering divisions from Arvind’s core textile business in H2 FY19 is expected to create value for the company’s shareholders. Verticalisation of the textile segment, promising prospects of the branded apparel segment and a healthy order book in the engineering segment reinforce our confidence in the stock.

However, risks linked to rising input costs, unfavourable revisions in license clauses (pertaining to foreign brands) and stiff competition from other major garment retailers could impact the financials materially. Moreover, Arvind’s omnichannel arm – ‘Arvind Internet’ (where products are sold through the nnnow.com website), despite comprising a small portion of the top-line, remains a loss-making segment.

Textile, Arvind’s largest segment, has been a laggard for quite some time. A performance turnaround on this front will, therefore, be pivotal in driving the next leg of profitability. Nonetheless, after a disappointing Q1 performance, at current levels, the stock leaves good room for an upside.

Thursday, 09 August 2018